By

![]() Checked by ,

Checked by ,

Updated

The Royal Mint's launch of DigiGold marked a significant step in modernising gold investment for a digital age, offering investors a simple, low-cost way to own fractional gold backed by the trusted physical reserves. Introduced to meet growing demand for accessible and flexible precious metal ownership, DigiGold enables customers to buy, sell, and hold digital portions of gold online without the need to take physical delivery. Since its launch, the product has gained strong traction among both new and experienced investors, reflecting growing appetite for secure, sovereign-backed digital gold solutions that combine the reliability of physical bullion with the convenience of online platforms.

Traditional saving methods

ISAs (Individual Savings Accounts) have been the traditional method of saving for many individuals for the last 20 years. They come in various forms, including; cash ISAs, junior cash ISAs, stocks and shares ISAs and lifetime ISAs, and they provide savers with a certain degree of taxation benefits.

Many people use ISAs because they are generally low risk; your money (up to a certain threshold) is kept in a bank or building society and no tax is paid on the interest that money accrues. ISAs are also covered by the Financial Services Compensation Scheme (FSCS), which protects savings up to £85,000, in the event of the failure of the ISA issuer.

A period of low interest rates (from 2009 to 2021) and rising inflation have hit traditional savings accounts such as ISAs. Whereas, economic uncertainty and political volatility has driven demand for gold globally, causing the value of gold to increase in response.

The rise of digital gold savings programmes

The Royal mint launched its DigiGold product back in 2015, and it has garnered huge interest from bullion investors, particularly given its eligibility to be held in pension schemes, namely SIPPs and SSASs.

Although not covered by the FSCS, this method of investing is particularly popular amongst individuals who wish to diversify their overall savings portfolio and those who wish to include gold within their holding without taking physical delivery of it.

To allay concerns around direct ownership, digital gold should always be backed by real, physical gold bars. By buying ‘digitally’ it allows you to buy a fraction or a portion of those physical gold bars at a time. At The Royal Mint, all of our digital gold is backed by LBMA-approved cast gold bars. The bars are fully insured and stored at our world-class vault facility, which is audited regularly by an independent third party.

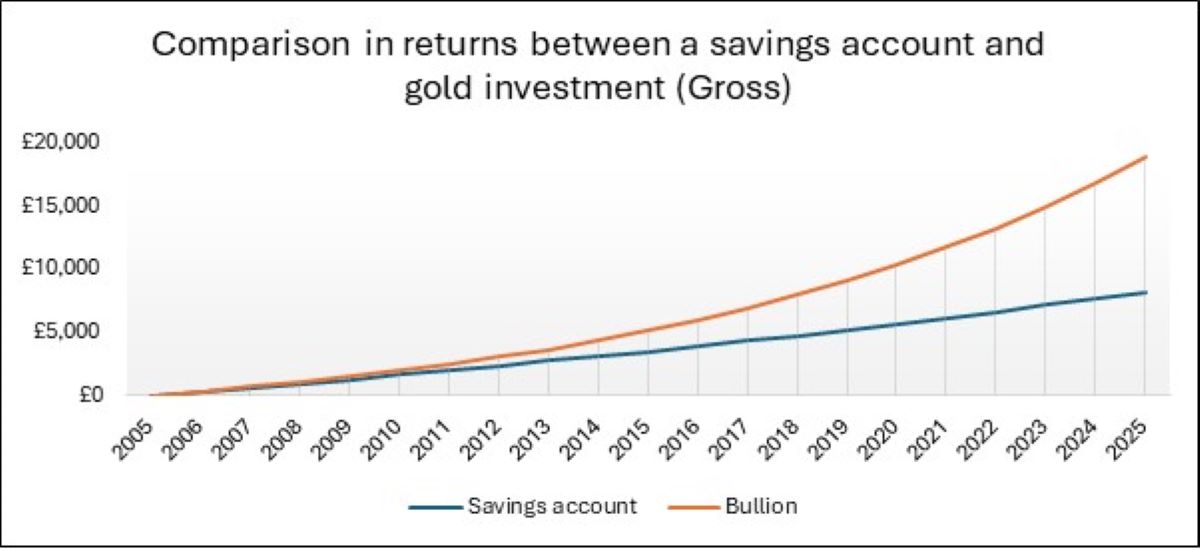

Long-term performance

In terms of performance, gold has achieved substantial gains over the last decade, providing a better yield than traditional savings options. Consider this; if you’d invested £25 a month in gold over 20 years between 2005 and 2025 (assuming average 10% return), you would have £18,985. Compare that with putting the same amount into a 3% cash ISA – you would have just £8,208 – or simply setting it aside with no interest at all – £6,000*.

*Calculated using an assumed 3% fixed interested rate (p.a.), with interest compounded monthly, for the ‘Savings account’. The ‘Bullion’ performance is compounded monthly, with an assumed average return of 10% p.a. All figures are gross of any transaction costs.

Regular payments

In the same way as regular cash ISAs, many gold savings programmes allow you to set up regular, recurring payments into your precious metals account. This allows you to buy and save gold every month as well as making one-off purchases whenever you choose. The minimum amount for the monthly payments is usually relatively small; at The Royal Mint it starts at just £25. Setting up regular savings by direct debit encourages a disciplined savings habit, and provides a lower average entry cost through a process known as ‘pound cost averaging’.

Digital gold savings and ISAs both attract various tax benefits but the risks and benefits associated with each are very different. While ISAs can benefit from exemptions in income tax and capital gains tax, gold is VAT free in the UK.

No upper limit

Unlike ISAs (which are capped at £20,000 per tax year) there is no upper limit to the amount of digital gold you can purchase. This provides opportunities for investors to take advantage of favourable market conditions whenever they arise.

No contractual tie in

Unlike fixed-term ISAs, which tie you in for a set period of time, digital gold affords you the flexibility to choose exactly when you want to buy and sell. There is no reliance on the banking system or other financial institutions as you are in complete control of the gold you own.

Redemption

An additional benefit with digital gold savings is that you can choose to sell your precious metal for cash whenever you want. You can also convert your holdings for physical gold coins and bars if you prefer; although there are usually additional fees (and potentially capital gains tax) associated with this option due to the design and manufacturing costs linked to these products.

Have you considered gold yet?

As rare as it is beautiful, gold has been used as a store of wealth for thousands of years. More recently, demand for investment gold has increased not only amongst individual investors but also amongst central banks, as governments have chosen to safeguard their national reserves.

The Royal Mint has a range of digital savings options available to cater for different needs:

- DigiGold: For those who wish to actively trade and save gold at the click of a button.

- Little Treasures: For parents, grandparents or guardians looking to set up a digital gold nest egg for their loves ones

- Gold for Pensions: For pension investors looking for a low-cost way to gain exposure to physical gold, and diversify away from traditional exchange trades securities

Precious metals markets can be volatile – the value of gold may fluctuate dependent on market value. Investing in gold involves a degree of risk which may make it unsuitable for certain people. Before making any investment decision, you may wish to seek advice from your financial, legal, tax and accounting advisers. You should carefully consider the risks associated with investing in gold taking into account your own individual financial needs and circumstances.

*The contents of this article are accurate at the time of publishing, are for general information purposes only and do not constitute investment, legal, tax or any other advice. Before making any investment or financial decision, you may wish to seek advice from your financial, legal, tax and/or accounting advisers